Installment Buying (Fixed)

- In this type of loan, the borrow agrees to pay a fixed number of payments which include principal and interest.

- This is not a simple interest loan.

- The terms of the loan include

- The principal or amount borrowed

- The interest rate

- The time.

- The number of payments per year.

- Examples of this type of loan include car loans, student loans, ...

- Any loan where you make a set number of regular payments.

- These do not include credit cards, as credit cards are open installment loans.

- The steps in these loans depend on the question.

- Sometimes you are asked to compute a down payment

- Sometimes you are asked to compute the amount financed which is the price - down payment.

- You normally need to compute the finance charge, which is the total amount of money the borrower must pay for using the principal.

- Sometimes you need to compute the monthly payment.

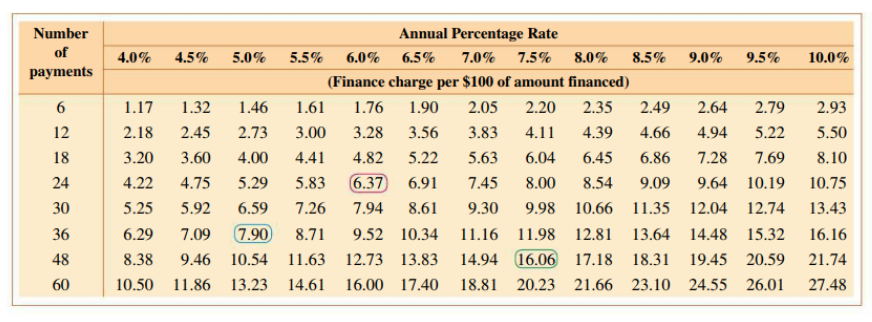

- Finance charges can be computed two ways

- The Installment payment formula

$$m = {p ({r \over n}) \over 1 - ( 1 + { r \over n}) ^ (-nt)}$$

- Or use the Annual Percentage Rate Table for Monthly Payment Plans

- I think, for our purposes, the second is easier.

- Do 7-10 page 602

- Do 11 or 12

- Sometimes you need to work backwards

- look at 13-16.

- Sometimes you want to pay off a loan early

- You need to compute unearned interest or interest that you don't need to pay

- $ u = {n p V \over 100+V} $

- u is unearned interest

- n is the number of payments remaining

- p is the monthly payment

- V is lookup n and r on the chart

- Payoff = this month + remaining months - unearned interest

- $ payoff = p + np -u $

- Look at 17-20