Chapter 2 of Excel

- I have somewhat of a schedule conflict on Thursday so

- I will be here for part of the day on Thursday and Dr. Meyer will be here for the rest.

- I will talk on both days.

- This section covers two things.

- Absolute vs relative vs mixed addressing.

- This is not hard, but rather a new skill most people need to learn

- Functions.

- This is both easy and hard.

- It is easy as the functions do the work for you.

- It is hard in that you need to learn the functions and when to use them.

- This is the page numbering thing all over, pay attention.

- Oh, and I would keep a list of functions, what they do and how to use them.

- Let's do a loan.

- Loans are the way we purchase many large items.

- Think car, boat, house, education, ...

- The loans we are talking about here are installment loans

- For a fixed period.

- Most loans require three pieces of input

- The amount borrowed.

- The period of the loan

- The interest rate of the loan.

- Sometimes we need to compute the down payment and amount financed.

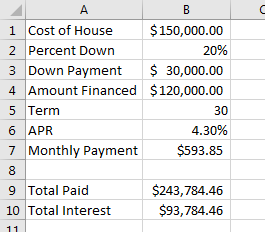

- Let's say we want to purchase a house for $150,000. We plan to pay for 30 years at an interest rate of 4.3%. The bank requires a 20% down payment.

- We want to do several things.

- Compute the monthly payment.

- Compute the amount of interest paid

- Compute the amortization table.

- Start by placing "cost of house" in a1 and $150,000 in B1

- Put Percent Down in A2 and 20% in B2

- Put Down Payment in A3

- Calculate the down payment in cell B3 (=b1*b2)

- Put Amount Financed in A4

- Calculate the amount financed in B4, (=b1-b3)

- Put "Term" in cell A5 and 30 in cell B5

- Put "APR" in cell A6 and 4.3% in cell B6.

- Put Payment in cell A7

- We are going to learn to use the payment function

- m = P(r/n)/(1-(1+r/n)^(-nt)) is the formula.

- But you will get this wrong.

- So excel has a payment function.

- It takes three parameters

- The monthly interest rate

- The number of payments

- The amount financed.

- We have a version of all three of these.

- The monthly interest rate is the APR (4.3%)/12

- The number of months is the term (30)*12

- The Amount financed is the -Amount financed.

- So in cell B7 put =pmt(b6/12, b5*12, -b4)

- End of discussion. Learn to do this, don't argue.

- Ok, two discussion points

- Sometimes you don't make monthly payments.

- In that case, don't divide and multiply by 12, but by the payments per year.

- Make sure that the term is given in years, not months, otherwise you don't need to multiply by 12.

- Let's calculate the total amount paid and the total interest paid.

- In cell A9 put Total Paid

- In cell B9 compute the total of all payments, don't forget to include the down payment. (=b7*b5*12+b3)

- In cell A10 put Total Interest

- In cell B10 compute the total interest (=b9-b1)

-

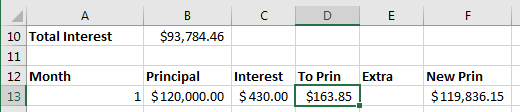

- We will now build an amortization table

- This shows you how the loan stands for each month.

- Across row 12 put the following

- Month

- Principal

- Interest

- To Prin

- Extra

- New Prin

-

- In column A, we want to place the month.

- Just put 1 in A13, 2 in A14, 3 in A15

- Highlight these three and drag down to A372.

- In column B we want to calculate the current amount due.

- This will be a two stage process. First just copy the amount from cell B4 (=b4) into B13

- We will do the next step later.

- In cell C13 we want to compute the interest due this month.

- This is a simple interest computation (i=prt)

- The principal is in cell b13.

- The interest rate is in cell B6, but this needs divided by 12

- The time is 1 month.

- So put the formula (=b13*b6/12) in cell c13

- We will modify this later.

- In Cell D13 we want to compute the part of the payment that goes toward principal.

- This is just the monthly payment (b7) minus the interest due this month (c13)

- In Cell D13 put (=b7-c13)

- We will change this later.

- E13 should be blank for now.

- In F13 we wish to compute the principal after the payment is made

- This is just the starting principal minus the amount to principal and any extra payment

- Enter (=B13-D13-E13) in cell F13

-

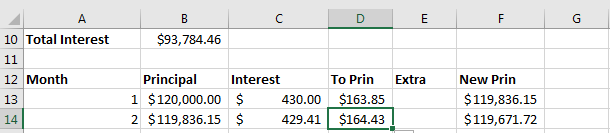

- We are now ready to compute row 14

- Where should the value for B14 come from (=F13)

- Can we copy the other formulas down?

- If I do, I owe $5,930,349.04 in interest, this does not seem right.

- Look at the formula

- =b14*b7/12

- This is using the monthly payment as the interest rate

- Why?

- Remember last time when we copied formulas in the checking book.

- If we copy a formula down the numbers go up.

- That is sort of what we want to happen here.

- We want the number associated with the principal to change from B13 to b14

- But we don't want the interest rate cell to change

- To keep this from happening, we can put a $ in front of the thing we don't want to change

- In this case, we don't want the 6 to change

- So the formula in cell C13 becomes (=b13*b$6/12)

- Copy that down and see what happens

- It works!

- So what modifications to we need to make to the formulas in cells D13 and F13? and WHY?

- D13 should become (=b$7-c13)

- F13 does not need to change.

- Copy these formulas down to row 14.

-

-

- We can now finish this table.

- Highlight cells b14:f14

- Double click in the box in the corner.

- The use of the $ in a formula changes the mode of addressing

- no $ is relative cell reference =b4-c2

- a $ in front of everything is a absolute cell reference =$b$3*$c$5

- Some $ and not some $ are called mixed references =b$3/$c5

- What happens when each of these is in cell d5 and copied to cell e6

- When do you put a $ in a cell reference

- By the way, F4 (the key) circles through the various options.